The U.S.$4bn Question: How Can Banks Unlock the Value of the Legal Entity Identifier (LEI)?

The banking industry has the potential to save billions in U.S. dollars annually by adopting LEIs more widely across their business. Where do financial institutions start?

Author: Stephan Wolf

Date: 2020-02-03

Views:

Of the many sectors that rely on counterparty identification and verification, GLEIF has identified banking as a key global sector in which scaling adoption of the Legal Entity Identifier (LEI) could create substantial and quantifiable value in the near to mid-term.

To see the results of a recent joint-report from GLEIF and McKinsey, download our eBook, or an infographic which outlines key findings here.

One of GLEIF’s key focuses for 2020 is to support voluntary adoption of the LEI in banking use cases, beyond regulatory reporting, so that significant benefits can be fully realized on a global scale.

How can banks alleviate client lifecycle issues while saving billions of dollars?

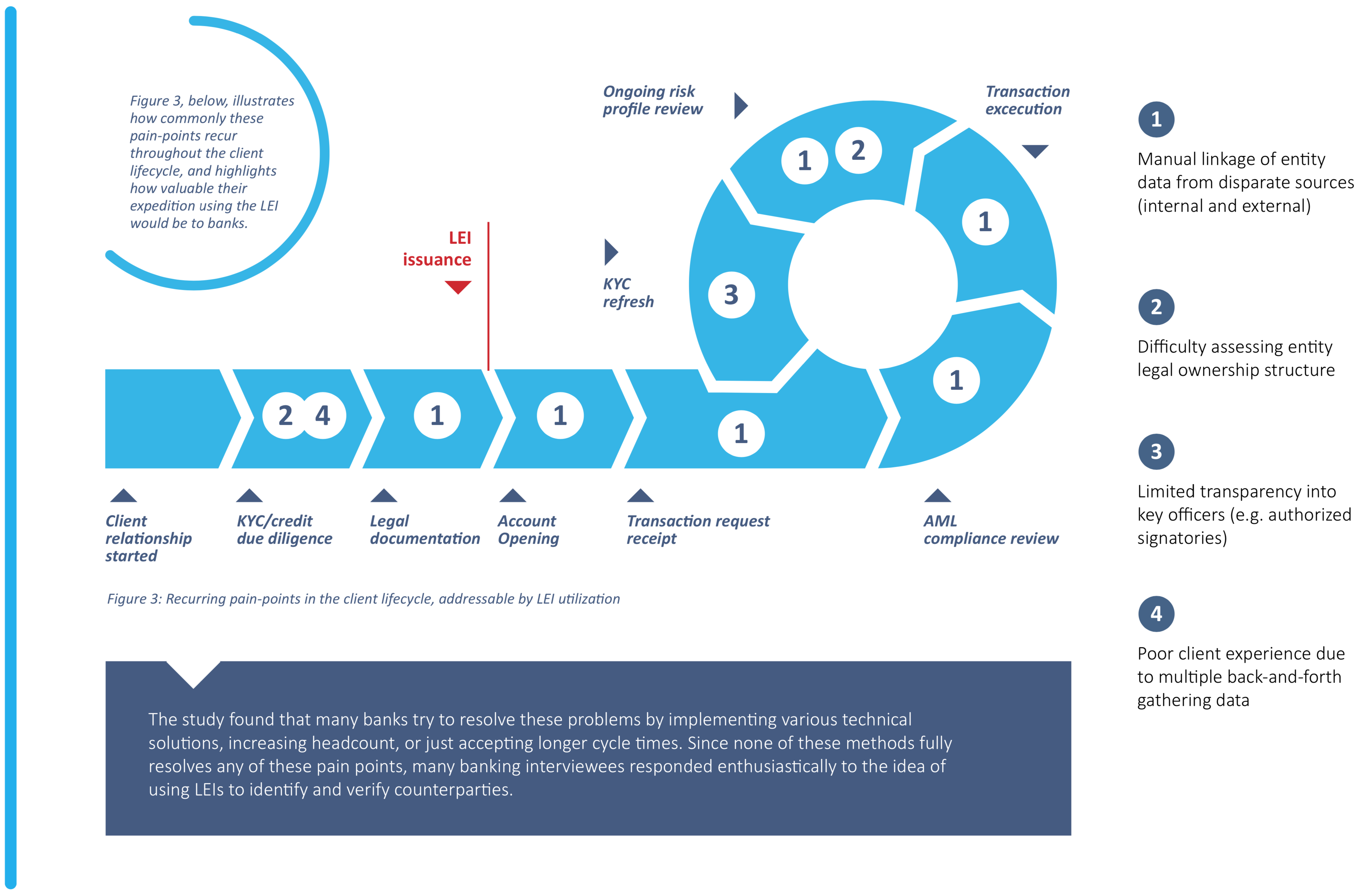

Client lifecycle management (CLM) is one use case where LEIs can address key pain points and dramatically simplify entity identification across different lifecycle stages – such as onboarding, transacting, compliance reporting and risk monitoring – at the same time as enhancing the all-important customer experience.

LEIs are already employed to streamline know-your-customer (KYC) processes in capital markets globally, so this is a good place for banks to begin the integration of LEIs. A recent joint-report from GLEIF and McKinsey revealed that wider use of LEIs across the global banking sector could save the industry U.S.$2-4 billion* annually in client onboarding costs alone. With estimated total industry spend on this area equal to U.S.$40 billion per year, productivity improvements gained through LEI usage could generate cross-sector cost reductions of between 5-10% annually.

The study identified four common pain points experienced by banks in relation to client identification and verification: manual linking of entity data from disparate internal and external sources; difficulties in assessing entities’ legal ownership structure; limited transparency into entities’ key officers, such as authorized signatories; and poor customer experience due to multiple round trips to gather client data and documents. Wider use of the LEI from the beginning of the onboarding process would enable banks to address these challenges head-on.

What other advantages could the LEI bring to client lifecycle management in banking?

The GLEIF and McKinsey research also lays out how LEIs can simplify entity identification in the digital age, which will unlock substantially more quantifiable value for banks in the near to mid-term.

In addition to delivering improved efficiencies and lower costs, widespread LEI usage can further generate topline benefits, such as between three to seven fewer days to revenue, improved client retention and a better customer experience, thanks to streamlined processes. The LEI could also help mitigate compliance and credit risk, as it gives banks more holistic views of clients across internal and external data sources.

A win-win situation

With so much to gain, banks should not delay making LEIs foundational to customer lifecycle management processes, not just in capital markets but across all banking business lines, such as trade financing, corporate banking and payments. Compliance driven adoption in capital markets means that banks are already familiar with the LEI. Voluntary expansion of LEI usage into other business banking lines is the new frontier in progressive thinking and can only lead to a win-win situation for both banks and their clients.

How can banks work with GLEIF to realize the value of LEI adoption?

As a next step, GLEIF is evaluating the feasibility of changes proposed by the McKinsey report, including an evolution of the Global Legal Entity Identifier System. GLEIF will also assess actions it can take to encourage banks to voluntarily adopt LEIs more broadly, such as enhancing the value proposition of the LEI by making it a data connector which links to the most commonly used data sources.

To ensure that the future evolution of the Global Legal Entity Identifier System is fully informed by, and in line with, the banking sector’s requirements, GLEIF aims to conduct its assessment on the report’s proposals with maximum engagement from the global banking community.

The GLEIF GIFI Relationship Group facilitates communication between GLEIF, banks, financial institutions and other key LEI stakeholders, making it possible for members to express their views on LEI services and for GLEIF to understand the requirements of LEI data users.

As GLEIF assesses the feasibility of proposals made in the report, direct interaction with banks is essential if we are to fully understand the needs of the sector and how GLEIF services and the Global Legal Entity Identifier System can best support it. We warmly welcome all interaction with banks and other financial institutions on this topic and would urge those interested in learning more to join the GLEIF GIFI Relationship Group for deeper insight and to ensure their voice is heard as we shape the future of the Global Legal Entity Identifier System together.

We are excited that wider use of the LEI brings such significant potential benefits to the banking sector and our priority at this stage is to support voluntary adoption of the LEI in banking use cases beyond regulatory reporting so that these benefits can be fully realized.

For further information on joining the GLEIF GIFI Relationship Group, please email info@gleif.org

* Source: McKinsey Cost per Trade Survey, Thomson Reuters "KYC Compliance: The Rising Challenge for Financial Institutions" report, GLEIS 2.0 voice of customer and expert interviews. McKinsey conducted a voice of the customer exercise involving interviews of over 70 stakeholders, including market participants across more than five sectors, current LEI registrants and users, Local Operating Units, regulators and potential Global LEI System partners.

Calculation: FTE productivity gain of (10% to 15% [~2-4 hours] of ~25 hours per onboarding case) multiplied by percentage of total onboarding costs attributable to FTEs (~57%) then multiplied by the estimated total industry spend on client onboarding ($40 billion per year). FTE productivity was based on “voice of customer” and expert interviews and includes both the estimated reduction and FTE hours per onboarding case. Percentage of total client onboarding costs attributable to FTEs based on the average cost of FTEs in the client onboarding function at 10 tier-1 banks (McKinsey Cost Per Trade Survey) divided by total client onboarding cost (European Association of Corporate Treasurers). Total industry client onboarding spend based on a Thomson Reuters report: KYC Compliance: The Rising Challenge for Financial Institutions.

If you would like to comment on a blog post, please identify yourself with your first and last name. Your name will appear next to your comment. Email addresses will not be published. Please note that by accessing or contributing to the discussion board you agree to abide by the terms of the GLEIF Blogging Policy, so please read them carefully.

Stephan Wolf was the CEO of the Global Legal Entity Identifier Foundation (GLEIF) (2014 - 2024). Since March 2024, he has led the International Chamber of Commerce (ICC)’s Industry Advisory Board (IAB) of the Digital Standards Initiative, the global platform for digital trade standards alignment, adoption, and engagement. Before he was appointed as Chair, he had been serving as Vice-Chair of the IAB since 2023. In the same year, he was elected to the Board of the International Chamber of Commerce (ICC) Germany.

Between January 2017 and June 2020, Mr. Wolf was Co-convener of the International Organization for Standardization Technical Committee 68 FinTech Technical Advisory Group (ISO TC 68 FinTech TAG). In January 2017, Mr. Wolf was named one of the Top 100 Leaders in Identity by One World Identity. He has extensive experience in establishing data operations and global implementation strategies. He has led the advancement of key business and product development strategies throughout his career. Mr. Wolf co-founded IS Innovative Software GmbH in 1989 and served first as its managing director. He was later named spokesman of the executive board of its successor, IS.Teledata AG. This company ultimately became part of Interactive Data Corporation, where Mr. Wolf held the role of CTO. Mr. Wolf holds a university degree in business administration from J. W. Goethe University, Frankfurt am Main.

{kind=link}

{kind=link}

{kind=link}